Palantir vs. SanDisk: Two Paths to AI Riches, One Winner

The post Palantir vs. SanDisk: Two Paths to AI Riches, One Winner appeared first on 24/7 Wall St..

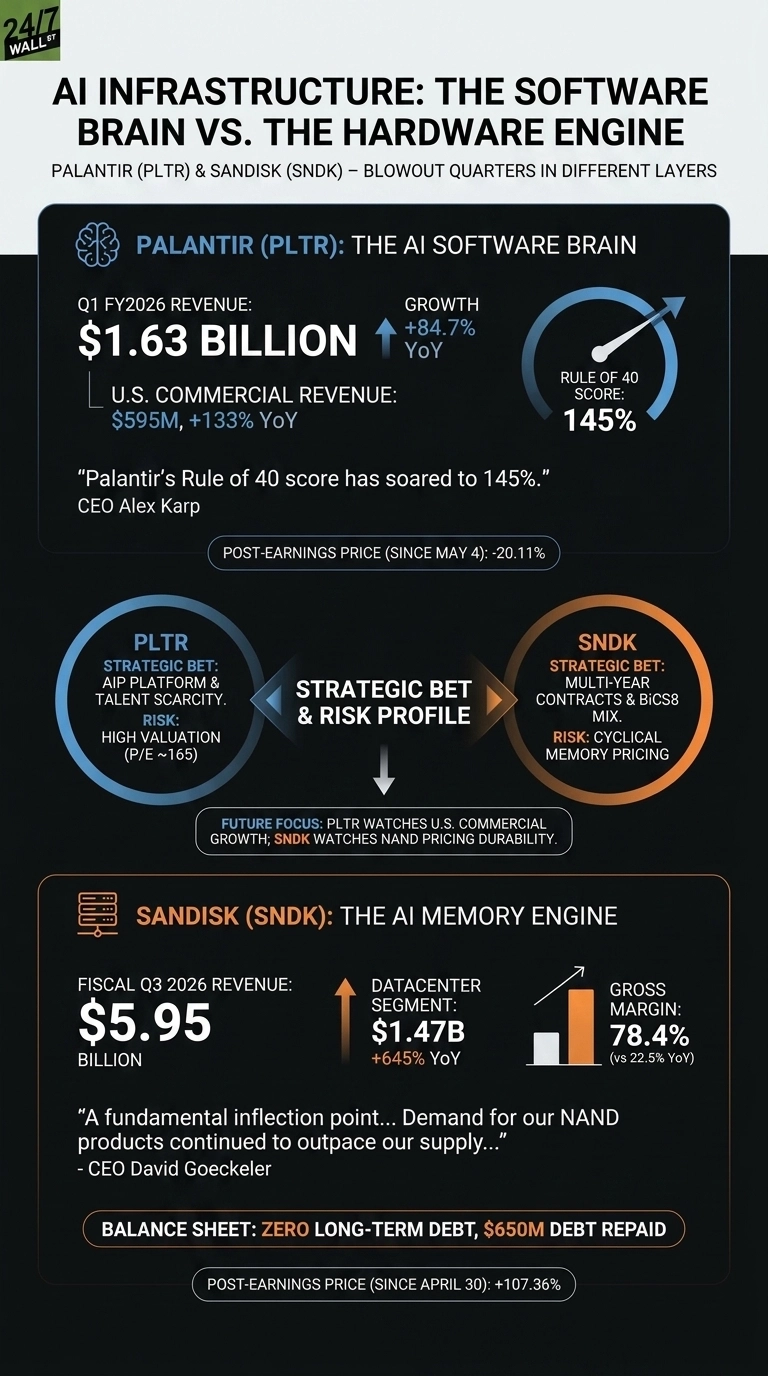

Palantir (NASDAQ: PLTR) and SanDisk (NASDAQ: SNDK) both posted blowout quarters, sitting on different rungs of the AI infrastructure ladder.

Palantir sells the software brain that runs enterprise AI. SanDisk sells the NAND flash memory that feeds hyperscaler datacenters. Comparing them shows how the AI buildout is minting winners at opposite ends of the stack.

AIP Lifts Palantir. NAND Pricing Lifts SanDisk.

Palantir’s Q1 FY2026 delivered adjusted EPS of $0.33 on revenue of $1.63 billion, up 84.71% year over year. U.S. commercial revenue jumped 133% to $595 million, driven by AIP adoption at customers like AIG, GE Aerospace, and Freedom Mortgage.

CEO Alex Karp framed the moment bluntly: “Palantir’s Rule of 40 score has soared to 145%.” That is elite software math.

SanDisk’s fiscal Q3 2026 was powered by hardware scarcity. Revenue hit $5.95 billion, and the Datacenter segment surged 645% year over year to $1.47 billion on AI memory buildout.

CEO David Goeckeler called it “a fundamental inflection point” as gross margin expanded to 78.4% from 22.5% a year earlier. Pricing drove the gains: “Demand for our NAND products continued to outpace our supply, a dynamic we expect to persist through the end of calendar year ’26 and beyond.”

24/7 Wall St.

24/7 Wall St.

Software Compounding vs. a Memory Supercycle

Palantir’s strategy leans on scarcity of talent and platform depth. CTO Shyam Sankar put it this way: “Tokens are the new coal; AIP is the train.” Management raised full-year 2026 revenue guidance to $7.65 billion to $7.662 billion, roughly 71% growth.

Shares trade at a P/E near 165, and stock-based comp hit $201.6 million in the quarter.

| Business Driver | Palantir | SanDisk |

| Main Growth Engine | AIP platform for enterprise AI | Datacenter NAND for hyperscalers |

| Management Focus | Ontology and agentic workflows | BiCS8 mix shift, multi-year commitments |

| Margin Character | Software (durable) | Cyclical (pricing-driven) |

SanDisk is pursuing durability through contracts. Goeckeler is converting quarterly buyers into multi-year customers via New Business Model agreements, having signed five NBM deals to date.

The balance sheet cleared: $650 million of debt repaid, zero long-term debt, and a buyback authorized. Q4 guidance calls for revenue of $7.75 to $8.25 billion and non-GAAP EPS of $30 to $33. Post-earnings, SNDK is up 107.36% since April 30, while PLTR has slid 20.11% since May 4 despite the beat.

What Decides the Next Quarter

For Palantir, watch whether U.S. commercial can hold triple-digit growth against the at least 120% bar management set. Karp admitted the constraint: “we just cannot meet demand.” Polymarket traders peg PLTR most likely in the $114 to $126 range through July, a modest recovery bet.

For SanDisk, the question is whether NAND pricing holds long enough for BiCS8 (now 15% of bits shipped) to lock in a structural cost advantage. If hyperscaler qualifications for the 128TB Stargate drive ramp on schedule in calendar year 2026, the cycle could stretch further than skeptics assume.

Where I Come Out on This Pair

The setup tilts toward SanDisk today. Rising prices, scarce supply, zero debt, and a fresh buyback reward patience. SanDisk offers steadier upside tied to the AI capex boom with a hardware moat.

Palantir remains the more visionary business, and its Rule of 40 is rare, but the multiple demands another two years of flawless execution.

For growth-oriented investors, PLTR’s platform-talent scarcity is the key variable to weigh against the multiple. Palantir would warrant a fresh research look if the stock retests support near $101, where prediction markets show 94.5% conviction on the floor holding.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Palantir didn’t make the cut. Grab the names FREE today.

The post Palantir vs. SanDisk: Two Paths to AI Riches, One Winner appeared first on 24/7 Wall St..

You May Also Like

Crypto News Roundup: Fresh Capital Floods Back as the Market Resets — Pepeto Presale Nears Its Binance Listing

BlackRock-backed Securitize puts its own shares onchain at debut