Take-Two Locked In GTA VI’s Launch Date. Now Comes the Hard Part

Key Stats for Take-Two Stock

- Current Price: $238.53

- Target Price (Mid): ~$440

- Street Target: ~$280

- Potential Total Return: ~83%

- Annualized Return to Target: ~14% / year

- Earnings Reaction: -4.42% (May 21, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Take-Two Interactive (TTWO) just got the one thing its shareholders have wanted for years: certainty. After a string of delays that turned Grand Theft Auto VI into a running joke on Wall Street, Rockstar Games confirmed the game launches on November 19, 2026, and opened preorders on June 25. The countdown is finally real.

So why did the stock sell off?

That is the tension worth sitting with. Shares ran up more than 13% over the surrounding week as anticipation built, with a roughly 3% to 5% pop when Rockstar set the preorder date on June 18. Then, when preorders actually opened and the pricing landed, the stock slipped around 3%, a textbook sell-the-news reaction. The standard edition came in at $79.99, not the $90 to $100 some investors had penciled in, and the launch is single-player only, with no confirmed date for the next version of GTA Online. For a stock trading near the top of its range at a valuation multiple far above its peers, “the date is set” was not enough. The market already assumed the date would be set.

The real question is no longer whether GTA VI ships. It is whether the biggest entertainment launch in history can still surprise a market that has spent two years pricing it in.

The Catalyst Investors Waited Years For

The numbers Rockstar attached to the launch are staggering even before a single copy sells. Grand Theft Auto has sold over 470 million units across the franchise’s history, and Bank of America estimates GTA VI alone will move 45 million units in fiscal 2027. Morningstar’s projection runs higher, at 60 to 70 million units in the launch year. Either figure would represent record digital distribution for the publisher.

Management has been blunt about what this title means. In its fiscal third-quarter results, the company said GTA VI would help “establish a new financial baseline” for the business, and at the fiscal 2026 year-end, it reaffirmed that fiscal 2027 will set new records driven by the November launch. That is the bet the stock is making: not a one-time spike, but a permanently higher floor.

The preorder details reinforce how deliberately Rockstar is building the on-ramp. Digital preorders bundle one month of GTA+, Rockstar’s subscription service, and a Vintage Vice City pack for early buyers. An Ultimate Edition runs $99.99. Preloading begins November 12, a full week before launch. Every piece is engineered to convert anticipation into day-one revenue, and to pull players toward recurring spending from the first session.

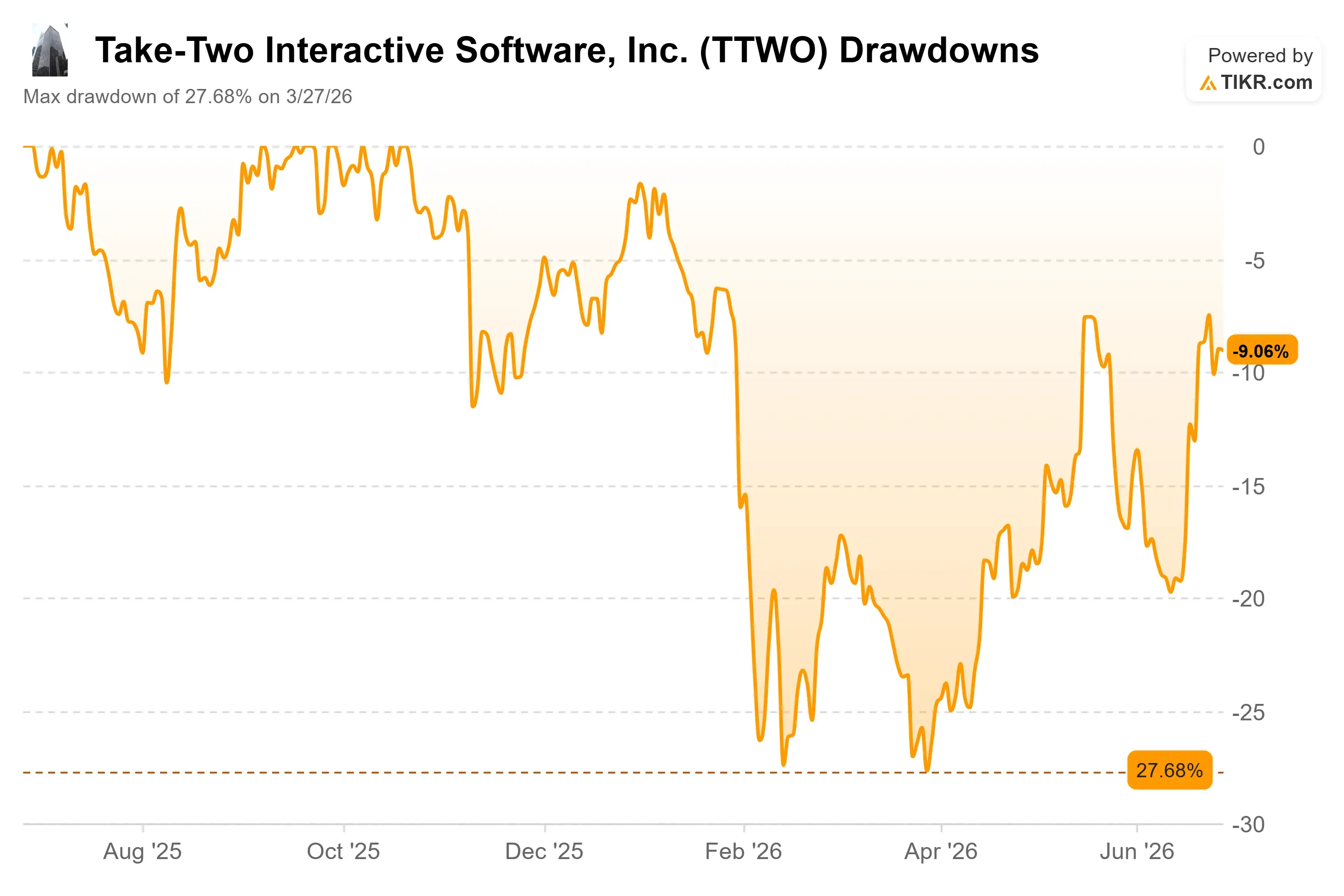

Take-Two Drawdowns (TIKR)

Take-Two Drawdowns (TIKR)

See historical and forward estimates for Take-Two stock (It’s free!) >>>

Why the Real Money Is Not the Game

Here is the part the headline price tag misses. The most important number in Take-Two’s fiscal 2026 results was not a unit count. It was 78%.

That is the share of total net bookings that came from recurrent consumer spending, meaning the in-game purchases, subscriptions, and virtual currency that players keep buying long after the box sale. Total net bookings rose 19% to $6.72 billion in fiscal 2026, with that recurring spend up 17%. The boxed game is now the trailer for the business, not the business itself.

This is why Bank of America’s Omar Dessouky raised his price target to $368 from $320 on June 23, the Street’s highest target. His thesis barely mentions launch units. Instead, he lifted his fiscal 2028 GTA Online bookings estimate to $2.2 billion and argued the new title “could monetize at 2x the predecessor, catching up to Fortnite.” The argument rests on a pay-to-progress model that drives higher per-player spending than a cosmetics-only approach. As a result, the durable earnings surprise, if it comes, arrives in the years after launch, not the launch quarter itself.

CEO Strauss Zelnick made the same point in his own language at the TD Cowen Technology, Media and Telecom Conference on May 27. Asked what Rockstar has learned about running live services, he kept it simple: “Give consumers something great and they show up for it. We’ve learned the oldest lesson in the entertainment business.” That confidence matters because the GTA ecosystem he is describing already exists. GTA Online, GTA+, and the FiveM business are generating recurring revenue today, before GTA VI adds a single player.

A Premium Valuation With No Margin for Error

None of this is cheap. TTWO trades at around 27 times NTM EV/EBITDA and roughly 35 times forward earnings, multiples that price the company for a launch that has not happened yet.

Set against its peer group, the premium is stark. Electronic Arts (NASDAQ: EA) trades at about 17 times NTM EV/EBITDA, and Netflix (NASDAQ: NFLX) sits near 18 times, both well below Take-Two. On a forward sales basis, the gap is wider still, with TTWO near 5 times next-twelve-month revenue against an entertainment peer median closer to 1 times. The market is paying up for one reason: no peer has a catalyst the size of GTA VI sitting six months out. Whether that premium is justified depends entirely on execution, because there is no valuation cushion if the launch slips.

The fundamentals underneath the launch are improving in the company’s favor. Take-Two has flipped from negative free cash flow in fiscal 2025 to positive free cash flow in fiscal 2026, and consensus models a sharp ramp as the launch quarter lands. The December 2026 quarter, which captures GTA VI’s first weeks, carries consensus revenue around $3.3 billion, an 86% jump over the prior year, with EBITDA margin expanding toward 27% from 19%. That is the inflection the whole thesis hangs on.

The risk sits in plain view. So much investor expectation is concentrated in fiscal 2027 and 2028 that any delay would hit harder than it would for almost any other stock. Zelnick himself acknowledged at TD Cowen that Rockstar takes as long as it needs, saying the gap between releases is driven by “the amount of time it takes to do something that is as good as it can possibly be.” Quality discipline is the franchise’s moat. It is also the source of the single risk that could break the trade.

Take-Two NTM EV/EBITDA (TIKR)

Take-Two NTM EV/EBITDA (TIKR)

See how Take-Two performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $238.53

- Target Price (Mid): ~$440

- Potential Total Return: ~83%

- Annualized Return to Target: ~14% / year

Take-Two Advanced Valuation Model (TIKR)

Take-Two Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Take-Two stock (It’s free!) >>>

Using TIKR’s mid-case scenario, the model points to a target of around $440 per share, implying roughly 83% total return and an annualized return near 14% per year through March 2031. The mid-case is the right anchor here because it assumes GTA VI succeeds without requiring the franchise to monetize at full Fortnite-level intensity, which keeps the forecast grounded in the company’s demonstrated track record rather than the bull-case dream.

Two drivers carry the revenue line. The first is the GTA VI launch wave itself, the unit sales, and digital deluxe upgrades that land in fiscal 2027. The second is the recurring spend ramp from GTA Online and GTA+, which the model expects to lift bookings durably in the years after launch. The margin driver is operating leverage: as that high-margin recurring revenue scales against a relatively fixed development base, net income margin expands toward around 21% in the mid case from single digits today.

The primary risk is timing. A launch delay or a soft GTA Online rollout would push the monetization ramp deeper into 2027 and reset the conviction baked into the current price. The upside case is that GTA VI monetizes at or above the company’s own GTA V playbook, and the recurring economy compounds for years. The downside case is that the $79.99 boxed price and a delayed online mode cap day-one momentum, and the premium multiple compresses before the recurring revenue arrives to justify it.

Conclusion

The date is locked, so the debate moves to a single question: Does GTA Online’s next version monetize the way the bulls claim? Watch the company’s fiscal first-quarter report in early August, the first earnings call since preorders opened. The number that matters is fiscal 2027 net bookings guidance and any commentary on GTA Online’s launch timing. Reaffirmed or raised guidance, plus a concrete online rollout window, would confirm the thesis. Softer guidance or continued silence on the online mode would signal that the market had gotten ahead of itself. After that, the real verdict comes with the December 2026 quarter, when the launch finally shows up in the numbers. Until then, Take-Two is a stock priced for a hit it has not yet delivered.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Take-Two?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Take-Two, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Take-Two alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Take-Two on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

George Conway and Mehdi Hasan deliver searing indictment of 'dumb' Trump’s presidency

BitMine Just 500K ETH Away From 5% Supply Goal

Exhibits at Trump’s State Fair documented by reporter: ‘Basically just put up some chairs’