Palantir Stock Is Down 31% Over the Past Year. Here’s Why the Army NGC2 Win Changes the Story

Key Stats for PLTR Stock

- Past week’s performance: -5.3%

- 52-week range: $40 to $80

- Valuation model target price: $247

- Implied upside: +130.1% over the next 2.5 years,

See how the Palantir valuation model was built on TIKR >>>

Palantir Locks In the Army, Expands Everywhere Else

Palantir Technologies (PLTR) closed a consequential stretch of news. The company secured a foundational role in the U.S. Army’s NGC2 common data layer baseline on June 23. NGC2, or Next Generation Command and Control, is the Army’s framework for integrating battlefield data across units, platforms, and domains. Palantir, partnering alongside Anduril, will serve as the underlying data infrastructure layer.

That win arrived amid a cluster of commercial expansions. Earlier in June, Palantir joined the Google Cloud Marketplace, opening a two-way integration between BigQuery and Foundry. Foundry is Palantir’s enterprise operating platform, which connects data, workflows, and AI models into a unified environment for large organizations. GNP Seguros, a major Mexican insurer, also announced a multiyear, multimillion-dollar expansion of Palantir Foundry and AIP across all business lines.

The commercial breadth widened further. Palantir partnered with construction firm McCarthy Building to deploy its AI platform across construction operations. Kirkland and Ellis, a leading law firm, launched an AI platform with Palantir focused on private equity fundraising workflows. These deals signal that Palantir’s AIP product, which stands for Artificial Intelligence Platform, is reaching into sectors well beyond defense and tech.

PLTR EBITDA (TIKR)

PLTR EBITDA (TIKR)

Not all headlines were positive. France’s domestic intelligence agency dropped Palantir in favor of a local rival. The UK government faced criticism for over-reliance on Palantir’s NHS contract. Yet sentiment among investors leaned toward the commercial acceleration story, especially after Q1 2026 revenue of $1.63 billion beat estimates of $1.54 billion by nearly 6%.

CEO Alex Karp said during the Q1 earnings call that demand for AIP had reached a point where “the U.S. commercial business is now the fastest-growing part of the company.” Going forward, whether PLTR stock re-rates meaningfully will depend on how fast that commercial book scales toward a recurring revenue base.

See analysts’ growth forecasts and price targets for PLTR (It’s free) >>>

Is Palantir Stock Undervalued at These Levels?

PLTR Guided Valuation Model (TIKR)

PLTR Guided Valuation Model (TIKR)

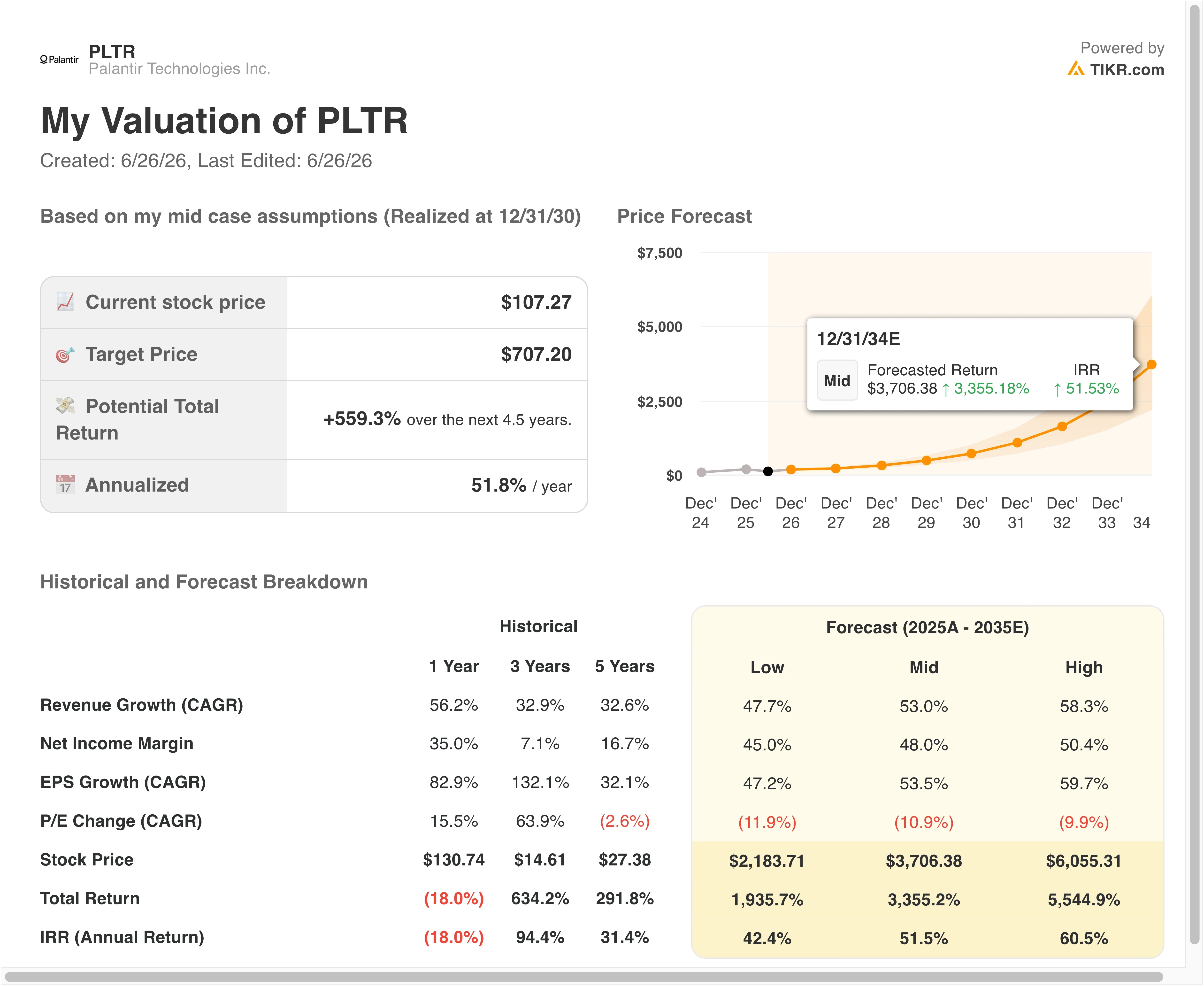

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 53%

- Operating Margins: 50.4%

- Exit P/E Multiple: 67.9x

Based on these inputs, the model estimates a target price of $247, implying 130.1% total upside from the current share price and a 39.2% annualized return over the next 2.5 years.

A 39.2% annualized return clears every threshold for what makes a stock genuinely interesting. But the assumptions behind that target are aggressive, and they deserve scrutiny. A 53% revenue CAGR through 2028 would require Palantir to roughly triple its top line in two and a half years. That trajectory is not impossible given recent Q1 momentum, but it demands consistent execution quarter after quarter.

PLTR Guided Valuation Model (TIKR)

PLTR Guided Valuation Model (TIKR)

The 50.4% operating margin assumption is particularly notable. Palantir’s LTM operating margin sits at 38.1% today, so reaching 50% would require meaningful scale benefits and disciplined cost control. The company already carries an 84.1% gross margin, which is software-level economics even inside a defense-heavy business. That underlying structure supports the idea that margins can expand as commercial revenue grows faster than headcount.

The 67.9x exit P/E multiple is the variable that most investors will debate. At current levels, PLTR trades at a trailing P/E above 120x. Reaching an exit multiple of 67.9x by the end of 2028 implies meaningful multiple compression even in the bull case. That compression is essentially “priced in” to the model, which shows the return depends entirely on earnings growth outrunning that multiple decline.

Compared to peers, Palantir’s premium reflects its unique positioning. CrowdStrike, a cybersecurity platform with strong government exposure, trades at roughly 70x forward earnings. Snowflake, a cloud data platform that competes in some enterprise analytics markets, trades near 60x. Palantir’s multiple still sits above both, but the gap has narrowed significantly after the past year’s drawdown.

Build your own Palantir valuation model on TIKR and stress-test the assumptions >>>

How Palantir Stacks Up Against the Competition

Palantir’s two most relevant comparisons in the AI and government software space are Palantir versus CrowdStrike on government exposure and Palantir versus Snowflake on commercial data platform growth.

CrowdStrike (CRWD) generated trailing revenue of roughly $3.9 billion, growing at a three-year CAGR near 35%. Its operating margins are improving, but still trail Palantir’s LTM EBIT margin of 38.1%. CrowdStrike trades at a forward NTM P/E near 70x, which is below where PLTR sits even after the drawdown.

PLTR Revenue vs SNOW and CRWD (TIKR)

PLTR Revenue vs SNOW and CRWD (TIKR)

Snowflake’s (SNOW) revenue trajectory is decelerating toward the low 20% range, and its path to GAAP profitability remains a discussion rather than a certainty. Snowflake’s NTM EV/Revenue multiple of roughly 12x to 14x compares favorably to PLTR’s 29.3x, but Snowflake lacks the government contract pipeline that gives Palantir its revenue floor.

The NGC2 win reinforces a core differentiator. Palantir is the only commercial software company with deep, active, classified integration at scale inside U.S. defense infrastructure. That moat is difficult to replicate and expensive to displace. So, while the valuation remains demanding, the competitive position justifies a structural premium over pure commercial SaaS peers.

Read why Palantir stock fell 6% despite a record Q1 beat (Full breakdown) >>>

What’s Driving Palantir Stock Going Forward?

The most important forward catalyst for Palantir is whether the U.S. commercial segment continues to accelerate. Q1 2026 showed U.S. commercial revenue growing above 70% year over year. That rate, sustained over several quarters, would be the single biggest driver of whether the model’s 53% revenue CAGR is achievable or aspirational.

The Google Cloud Marketplace integration is strategically significant. Because Google Cloud is used by thousands of large enterprises, Palantir’s Foundry being natively available in that environment lowers the procurement barrier substantially. Enterprise software buyers often prefer to buy through existing cloud vendor relationships, so this distribution move could accelerate deal cycles for new commercial customers.

On the government side, the NGC2 win matters beyond its contract value. Palantir has now established itself as the foundational data layer for a major modernization program inside the U.S. Army. Being the baseline infrastructure provider in a multi-year government program creates durable, hard-to-displace revenue that de-risks the commercial growth story from a balance sheet perspective.

The UK NHS contract review and France’s decision to exit Palantir’s platform are reminders that international government revenue carries geopolitical risk. Neither development changes the near-term revenue outlook, but they signal that European public sector contracts may be harder to grow than domestic U.S. ones. Palantir’s Q2 2026 results, expected on August 3, will be the next major catalyst to watch.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Palantir?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PLTR, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PLTR alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze PLTR stock on TIKR Free→

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Republicans 'can’t escape' their 'abusive marriage' with Trump: DC insider

Malaysian Ringgit: Policy Support Tempers Downside but Caps Upside, Says MUFG

U.S. Regulation of ChatGPT Turns Washington Into AI Gatekeeper