Open USD Stablecoin (OUSD): Why the New Stablecoin Alliance Matters

Open USD Stablecoin, also referred to as OUSD, has quickly become one of the most important stablecoin stories of 2026. Unlike many new digital assets that begin inside a small crypto-native community, Open USD is being built around a large payments, technology, financial-services, and crypto consortium. Reported participants include major names across cards, fintech, asset management, cloud infrastructure, and blockchain networks.

That makes OUSD different from a typical stablecoin launch. The market is not only watching whether the token can maintain a dollar peg. It is watching whether a large group of mainstream companies can create a stablecoin distribution network strong enough to challenge USDC, USDT, and the existing stablecoin revenue model.

The short version: Open USD is not just another dollar token. If it launches successfully, it could become a major test of whether stablecoins move from crypto trading infrastructure into mainstream payments, settlement, and enterprise finance. But it is still early, and traders should avoid treating future adoption as guaranteed.

What Is Open USD Stablecoin?

Open USD Stablecoin is a planned U.S. dollar-backed stablecoin from Open Standard. Public reports describe it as a new stablecoin network supported by more than 140 businesses, including major payments companies, financial institutions, technology firms, and crypto companies.

The goal appears to be simple but ambitious: create a dollar stablecoin that is open, low-cost, widely distributed, and aligned with the companies that use it. Instead of one issuer capturing most reserve income, Open USD is expected to share reserve earnings with participating adopters after operational costs.

That model is important because stablecoin economics are powerful. When users hold dollar-backed stablecoins, the reserves backing those tokens are usually held in cash, short-term Treasury bills, or similar low-risk assets. Those reserves can generate yield. For large stablecoin issuers, reserve income can become a major revenue source.

Open USD’s reported structure tries to make that revenue model more attractive to distribution partners. If payment companies, fintech apps, exchanges, wallets, and enterprise platforms can share in the economics, they may have a stronger incentive to integrate OUSD into their systems.

Why OUSD Is Getting So Much Attention

Stablecoins have already become one of crypto’s most practical use cases. They are used for trading, settlement, remittances, treasury management, cross-border transfers, and dollar access in markets where banking infrastructure is limited or local currency volatility is high.

But the market has been highly concentrated. USDT and USDC dominate most stablecoin activity. USDT is especially strong in global crypto trading, while USDC has been important for regulated U.S.-linked crypto infrastructure and institutional use cases.

Open USD matters because it may challenge that concentration from a different angle. Instead of trying to win only through crypto exchange liquidity, it may start with distribution. If major payments and technology companies integrate the same stablecoin, adoption could come from wallets, merchant systems, corporate payments, cross-border flows, and tokenized financial products.

That is why the announcement affected public-market sentiment around stablecoin-related companies. If OUSD becomes a real competitor, the market may need to reassess how much pricing power existing stablecoin issuers can keep.

For readers monitoring broader digital-asset markets, MEXC Marketscan be used to follow crypto market activity and stablecoin-related trading conditions.

Open USD vs USDC and USDT

The biggest question is whether Open USD can compete with USDC and USDT.

USDT has the deepest role in global crypto trading. It benefits from liquidity, habit, exchange support, and broad international usage. USDC has a stronger U.S. regulatory and institutional identity, and it has become important across centralized exchanges, DeFi, fintech apps, and corporate crypto infrastructure.

Open USD may not need to replace either one immediately. Its first realistic goal may be to become a preferred stablecoin for companies that want a more open revenue-sharing model and deeper alignment between issuers and distributors.

That is a different competitive strategy. USDT and USDC won by becoming trusted and liquid. Open USD may try to win by becoming useful to large platforms before retail users even think about it.

Still, liquidity is hard to build. A stablecoin needs deep markets, reliable redemption, strong reserve transparency, broad exchange support, wallet support, merchant support, and user trust. Distribution partners can help, but they do not automatically create market depth.

The Business Model: Why Reserve Income Matters

The most important financial detail behind Open USD is reserve income.

A dollar-backed stablecoin normally issues tokens when users deposit dollars or equivalent assets. Those reserves are then held in safe instruments. When interest rates are meaningful, reserve assets can produce substantial income.

That income has become a key part of the stablecoin business. For companies tied closely to stablecoin reserves, higher stablecoin supply can mean higher revenue. This is why investors pay attention to stablecoin circulation, redemption trends, interest rates, and market share.

Open USD’s reported model would share reserve earnings with adopters after costs. That could be disruptive. If major platforms can earn from helping distribute and use OUSD, they may prefer it over stablecoins where most economics accrue to a separate issuer.

But this also creates questions. How will revenue be split? Who controls reserves? What assets will back OUSD? How transparent will reporting be? Which jurisdictions will apply? How will users redeem? What happens if interest rates fall and reserve income shrinks?

These details will matter more than the announcement itself.

Regulation Could Be a Tailwind and a Constraint

Stablecoin regulation has become a major market theme. Clearer rules can help institutional adoption because banks, payment companies, and corporate users need legal certainty before they build around blockchain settlement.

For Open USD, regulation could be a tailwind if it gives large companies confidence to use stablecoins in real payment flows. A clearer legal framework may make stablecoins more acceptable for settlement, treasury, and consumer payment use cases.

But regulation is also a constraint. A stablecoin backed by mainstream companies will face high expectations around reserves, audits, redemption rights, compliance, sanctions screening, consumer protection, and operational risk.

That means OUSD may have to move more carefully than smaller crypto-native stablecoins. The trade-off is clear: mainstream credibility may bring adoption, but it also brings more oversight.

For users who want to understand crypto-market basics, stablecoin mechanics, and risk management, MEXC Learncan be a useful starting point.

Bull Case, Base Case, Bear Case

Bull case:Open USD launches smoothly, gains support across major payment and fintech platforms, and becomes a serious alternative to USDC and USDT. Its revenue-sharing structure gives partners a strong incentive to promote usage. In this scenario, OUSD could become one of the most important new stablecoins in the market.

Base case:OUSD launches with strong brand support but adoption grows gradually. It gains some enterprise and payment use cases, but USDT and USDC remain dominant in crypto trading and DeFi liquidity. Open USD becomes relevant, but not immediately market-changing.

Bear case:The launch is delayed, regulatory requirements slow adoption, liquidity remains thin, or partners integrate OUSD cautiously. If users do not see a clear advantage over existing stablecoins, Open USD may struggle despite strong backers.

What Traders Usually Miss

The biggest mistake is assuming that a large partner list guarantees adoption. In stablecoins, distribution matters, but trust and liquidity matter just as much.

A user will not hold a stablecoin simply because many companies joined an alliance. They need confidence that the token is redeemable, transparent, liquid, and accepted where they want to use it. Merchants and businesses need reliability. Exchanges need market depth. Institutions need compliance. Developers need predictable infrastructure.

Another mistake is confusing Open USD with other assets using the OUSD ticker. There are existing crypto projects that use similar names or tickers, including Origin Dollar. Open USD Stablecoin should be evaluated separately from those assets. Before trading or referencing any token, users should verify the contract, issuer, network, and official listing information.

The third mistake is treating stablecoins as risk-free. A stablecoin can be designed to maintain a one-dollar value, but it still carries issuer risk, reserve risk, liquidity risk, regulatory risk, smart-contract risk, operational risk, and market-confidence risk.

What to Watch Next

The first thing to watch is the official launch timeline. Reports indicate Open USD is expected later in 2026, but traders should wait for confirmed issuer details, supported networks, redemption terms, and official documentation.

The second thing to watch is reserve transparency. Stablecoin users should look for clear reporting on reserve assets, custody, audits, redemption rights, and risk controls.

The third signal is exchange and wallet support. A stablecoin becomes more useful when it is easy to trade, transfer, store, and redeem.

The fourth signal is real payment usage. If OUSD appears in merchant payments, cross-border transfers, fintech apps, corporate settlement, and tokenized finance, the adoption case becomes stronger.

The fifth signal is the response from USDC and USDT. Existing leaders may adjust pricing, partnerships, incentives, or infrastructure to defend market share.

Bottom Line

Open USD Stablecoin could become one of the most important stablecoin launches of 2026 because it is backed by a broad alliance of payments, technology, financial, and crypto companies. Its reported revenue-sharing model also challenges how the stablecoin business has traditionally worked.

The opportunity is clear: if OUSD combines strong distribution, transparent reserves, low-cost minting and redemption, and real payment utility, it could become a serious competitor in the dollar-stablecoin market.

The risk is also clear: stablecoin adoption is not guaranteed by announcements. OUSD still needs liquidity, trust, regulatory clarity, exchange support, wallet support, and real user demand.

For now, Open USD should be viewed as a major stablecoin development to watch, not as a proven replacement for USDC or USDT.

FAQ

What is Open USD Stablecoin?

Open USD Stablecoin, or OUSD, is a planned dollar-backed stablecoin from Open Standard, supported by a large consortium of payments, technology, financial, and crypto companies.

Is Open USD already trading?

Public reports describe Open USD as expected to launch later in 2026. Users should verify official listings and contract details before interacting with any token using the OUSD name.

How is Open USD different from USDC?

Open USD is expected to use a more open consortium model, with reserve earnings shared among adopters after costs. USDC is an established stablecoin with deep institutional and crypto-market adoption.

Is OUSD the same as Origin Dollar?

No. Open USD Stablecoin should not be confused with Origin Dollar, which also uses the OUSD ticker in DeFi. Always verify the issuer and contract before trading.

What is the biggest risk with Open USD?

The biggest risks are launch execution, reserve transparency, regulatory compliance, liquidity, redemption reliability, and whether partner support turns into real user adoption.

Risk Warning

This article is for informational purposes only and should not be considered financial advice. Stablecoins can carry issuer risk, reserve risk, liquidity risk, regulatory risk, smart-contract risk, operational risk, and market-confidence risk. Open USD is still an emerging stablecoin initiative, and users should verify official documentation, supported networks, contract addresses, and product availability before making any trading or investment decision.

Popular Articles

View More

Will Europe's Digital Euro Kill the Stablecoin Market? CBDC vs. Bitcoin vs. USDC

On June 23, 2026, the European Parliament's Economic and Monetary Affairs Committee voted to approve the legal framework for a digital euro. What makes the timing extraordinary is what happened

What Is Solana Pay? How It Works and Where You Can Use It

Crypto payments are gaining traction in mainstream commerce, with platforms like Shopify now offering blockchain-based checkout options. This article breaks down everything you need to know about

Ethereum Network: What It Is, How It Works, and Why It Matters

The Ethereum network is one of the most important technologies in crypto — and it does far more than move money. Whether you're curious about what powers USDT and USDC, how smart contracts work, or

USD1 Stablecoin In-Depth Comparison: Comprehensive Analysis of Differences and Similarities with USDC, USDT, and USDS

Key Takeaways USD1, USDC, USDT, and USDS are all stablecoins pegged to the US dollar, designed to maintain a 1:1 price anchor These four stablecoins differ significantly in issuance mechanisms,

Hot Crypto Updates

View More

RLUSD, USDe, and USD1: The New Stablecoin Race Heating Up Crypto Markets

For years, the stablecoin market was largely dominated by two names: USDT and USDC. These dollar-pegged digital assets became essential tools for traders, investors, and businesses seeking stability

Coinbase Just Turned Stablecoin Issuance Into a Product — USDF Is the Proof

Coinbase and Flipcash have launched USDF, a custom USDC-backed stablecoin on Solana, marking the first live deployment on Coinbase's stablecoin-as-a-service platform. Here's what it means for crypto

Why Millions Are Fleeing Fiat for USDT & USDC in 2026

Millions of people across Argentina, Turkey, Venezuela, and Nigeria are ditching local currencies for USDT and USDC. Here's the data-backed breakdown of why — and what it means for the future of

Trending News

View More

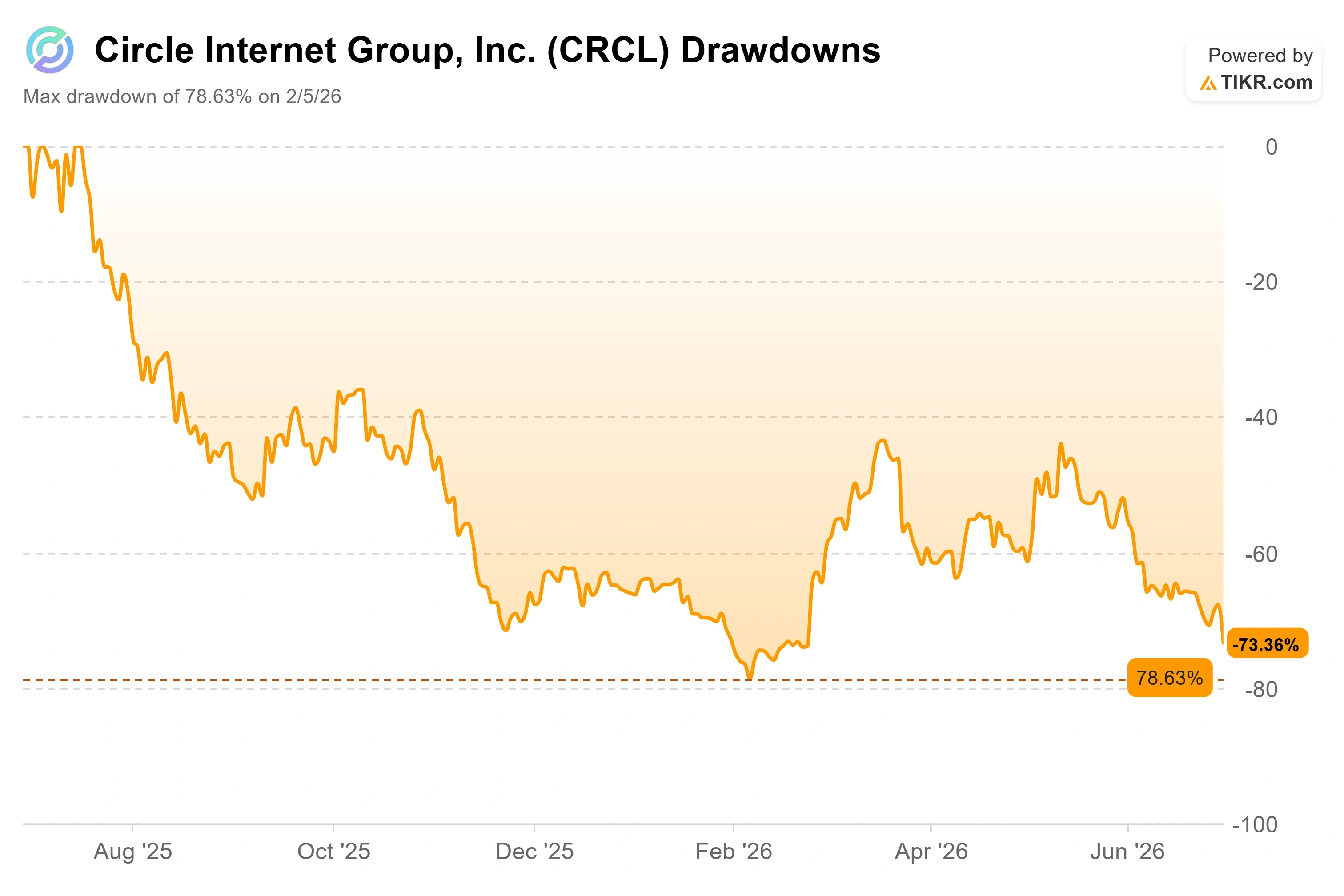

Circle Stock Fell 18% After a Rival Stablecoin Launched: Is CRCL a Buy at $62?

Circle’s own partners just backed a stablecoin built to take USDC’s economics apart, and the stock lost nearly a fifth of its value in a day. The selloff is either

Circle Mints Another $1B USDC on Solana, 2026 Total Hits $64.25B

Circle Mints Another $1 Billion USDC on Solana, Total 2026 Issuance Reaches $64.25 Billion Circle has minted another $1 billion worth of USD Coin (USDC) on the

Related Articles

View More

DJT Stock: Is Trump Media a Turnaround Trade or a Political Meme Stock?

DJT stock is one of the strangest names in the U.S. equity market. Trump Media & Technology Group, the company behind Truth Social, trades like a media company, a political proxy, a meme stock, a cryp

Trump Meme Coin: What Traders Should Know About TRUMP, Politics, and Meme-Coin Risk

Trump meme coin is not a normal crypto asset. It is part meme coin, part political brand, part speculative trading vehicle, and part controversy. Since its launch in January 2025, TRUMP has become one

Anthropic Fable 5: Why the New AI Model Matters for Investors

Anthropic Fable 5 is quickly becoming more than a technology headline. For investors, it sits at the center of several powerful market themes: frontier AI competition, U.S. regulation, cloud infrastru