Dell Nearing 52-Week High: Buy, Sell or Hold?

The post Dell Nearing 52-Week High: Buy, Sell or Hold? appeared first on 24/7 Wall St..

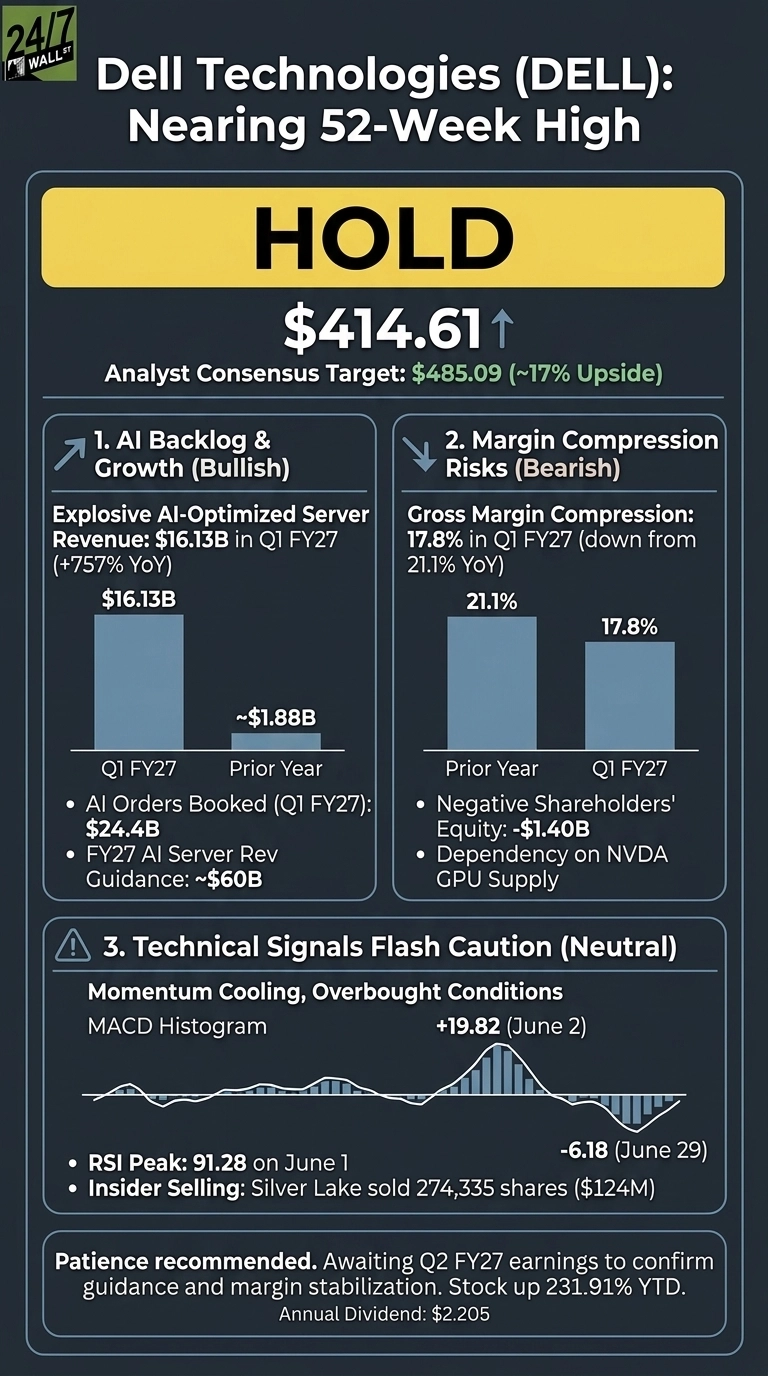

- Dell (DELL) at $414.61 is a Hold after tripling; risk/reward no longer favors buying.

- Dell's AI-server revenue surged 757% YoY to $16.13 billion, justifying the elevated multiple.

- Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Dell Technologies didn't make the cut. Grab the names FREE today.

Dell Technologies (NYSE:DELL) at $414.61 is a hold. The stock has tripled in six months on AI server demand, and with shares sitting just below a 52-week high of $469.47, the risk/reward is no longer one-sided.

Dell is the world’s largest enterprise server vendor and dominant force in commercial PCs, now the go-to integrator for AI infrastructure. Its Infrastructure Solutions Group sells GPU-packed servers that hyperscalers and enterprises buy to train and serve models. The Client Solutions Group anchors the business with commercial PCs and steady refresh cycles.

Shares are up 231.91% year to date and 239.58% over twelve months, fueled by an AI-server pipeline outrunning expectations.

Why the AI Backlog Justifies the Multiple

Q1 FY27 was a blowout. Revenue hit $43.84 billion, up 87.54% year over year, with non-GAAP EPS of $4.86 against a $2.96 estimate. AI-optimized server revenue reached $16.13 billion, up 757% YoY, and Dell booked $24.4 billion in AI orders during the quarter.

Management raised FY27 guidance to $165 billion to $169 billion in revenue, with AI servers tracking to $60 billion and non-GAAP EPS at a $17.90 midpoint, up 74%. On forward earnings, the 21x forward P/E looks reasonable.

Morgan Stanley lifted its price target to $477, and the company is returning capital aggressively with a 20% dividend hike and $10 billion buyback expansion.

Why the Margin Math Should Worry Bulls

The AI mix is diluting profitability. Gross margin compressed to 17.8% from 21.1% year over year, a structural shift as low-margin GPU servers crowd out higher-margin storage. The balance sheet carries negative shareholders’ equity of -$1.40 billion, and Dell depends on NVIDIA (NASDAQ:NVDA)-allocated GPUs to fulfill its backlog.

Both cases are credible. The backlog is real, but so is margin compression. The buyback is real, but so is insider selling. Dell needs to deliver on its Q2 FY27 guide of $44 billion to $45 billion and show ISG margin holding above 10% before chasing this rally makes sense.

The Numbers Behind the Setup

Shares trade at $414.61 against a consensus target of $485.09, implying roughly 17% upside. Of 26 analysts, 5 rate Strong Buy, 13 Buy, 7 Hold, and 1 Sell. The trailing P/E is 32, forward P/E 22.

Dell is up 231.91% YTD while the S&P 500 delivered low double-digit gains over the same stretch. The 50-day moving average sits at $305.90, the 200-day at $180.96, evidence of how vertical this move has been.

24/7 Wall St.

24/7 Wall St.

At $414.61, Dell Is a Hold

After a 240% twelve-month rip, the upside to consensus is roughly 17%, while a single quarter of AI order softness or gross-margin slippage below 17% could compress the multiple by more than that. The reward no longer pays for the risk at this entry.

Triggers for a Buy: a Q2 earnings report confirming the $44 billion to $45 billion guide, ISG operating margin holding above 10%, and AI backlog growth matching shipments. A clean beat in late August would change the math. Softness in AI orders, hyperscaler capex deceleration, or a bearish MACD crossover would tip this toward Sell.

Dell pays a $2.205 annual dividend while you wait, and the next earnings report arrives in roughly two months. When a stock has tripled and momentum is rolling over, let the next quarter do the talking.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Dell Technologies didn’t make the cut. Grab the names FREE today.

The post Dell Nearing 52-Week High: Buy, Sell or Hold? appeared first on 24/7 Wall St..

You May Also Like

Ethereum Institutional launched to boost Wall Street adoption after foundation layoffs

Bitcoin Exchange Binance Announces New Listings on its Futures Platform! Here Are the Details